We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Aug 10, 2020 / News

Changes to minimum pension payments

As part of the Government’s commitment to Australians during COVID-19 crisis, it recently announced changes to the minimum pension payments for retirees.

The minimum pension drawdown rates have been halved for the 2019/20 and 2020/21 financial years. This action is in response to dramatic movements in global share markets, which have seen many people’s superannuation balances fall.

How does this benefit me?

This change to minimum pension payments is welcome news for retirees with account-based pensions, market-linked pensions and transition to retirement pensions.

It will offer flexibility for retirees, who won’t now be forced to sell their shares, property or other assets at a time when their value is reduced simply to fund their income stream.

Instead, if they have sufficient ongoing cash flow to meet day-to-day living expenses, retirees will be able to ride out the current volatility and avoid capitalising any losses by keeping more of their money invested. When the sharemarket recovers, they’ll also be well positioned to take advantage of any opportunities that brings.

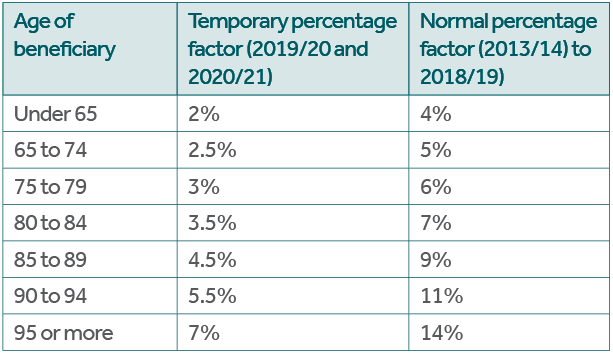

New minimum pension drawdown rates

What is an account-based pension?

An account-based pension offers retirees regular, flexible and tax-effective income from their superannuation account. You might also see it referred to as an allocated pension.

Members of a Self-Managed Super Fund can also have an account-based pension, provided the payment is allocated to a separate account for each member of the fund.

You can access an account-based pension once you reach your ‘preservation age’ (between 55 and 60 based on when you were born) with just a few simple choices1.

- Decide how much you want to transfer to the pension phase.

- Choose the frequency of your payments monthly, quarterly, half-yearly or annually.

- Choose the amount you want to receive in each payment (subject to minimum and maximum requirements).

- Consider how you want the remainder of your superannuation to continue to be invested so it keeps working hard for you.

While the pension income isn’t guaranteed for life, the income stream will continue for as long as your accumulated superannuation money does.

Why is there a minimum pension payment?

The Government sets minimum pension payment rules for just one simple reason – to satisfy the sole purpose test.

The sole purpose test requires that all activities of super funds must be for the sole purpose of providing retirement benefits to their members2.

It prevents super funds and their members from taking advantage of the attractive tax concessions and using superannuation as a way to transfer wealth to the next generation.

The rules

Pension amount

The minimum pension drawdown rates are calculated as an annual percentage of your account balance.

This percentage amount increases with age and is based on assumptions around what’s considered a sensible amount to withdraw annually while maintaining an account balance that’s enough for you to draw an income throughout retirement2.

Each year, the minimum amount you will receive is recalculated based on your age and account balance as at 1 July. If you open a new pension account part way through a financial year, the minimum pension drawdown rate is pro-rated and calculated based on the number of days left until the end of the financial year.

Pension frequency

You can choose whether you want to receive pension payments monthly, quarterly, half- yearly or annually – whichever suits your individual circumstances.

But it’s a condition of all account-based pensions that you must receive at least one pension payment annually between 1 July and 30 June each financial year.

How can I adjust my minimum pension payment?

We’ve updated all our systems to take account of the new reduced pension minimums.

How can Edwards Marshall Financial Solutions help you?

So, if you’re worried that your superannuation balance has been impacted by recent share market volatility and you would like to change your minimum pension drawdown amount to take advantage of the temporary reduction in rates, we recommend you speak to your financial adviser. They can work with you to ensure your investments are structured in the best way to help you achieve your longer-term retirement goals while still providing you with adequate income for daily essentials1.

About us

EMFS was formed in 2001 originally to service the financial planning needs of the clients of Nexia Edwards Marshall, Chartered Accountants. In addition, we now service clients referred by other accounting firms, lawyers and clients who are not serviced by Nexia Edwards Marshall. We manage funds totalling about $250m on behalf of clients.

1 - Moneysmart Moneysmart.gov.au https://moneysmart.gov.au/retirement-income/account-based-pensions

2 - SuperGuide https://www.superguide.com.au/smsfs/what-is-the-sole-purpose-test-and-how-does-it-work

Liability limited by a scheme approved under Professional Standards Legislation. Contents of this publication are general of nature and are not intended to be used for decision making purposes. Edwards Marshall Financial Solutions Pty Ltd ABN 45 096 434 842 is an Authorised Representative of Edwards Marshall Advisory Pty Ltd ABN 18 600 878 555. AFS Licence No. 479 792.