We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Jan 23, 2024 / News

Draft legislation for climate-related disclosures issued

The Treasury has released its Climate-related financial disclosure: exposure draft legislation.

The draft legislation introduces mandated climate-related financial disclosures in a separate sustainability report forming part of an entities’ annual report. Entities will also be required to obtain an assurance report over the sustainability report from their financial auditors.

Summary

- Reporting entities: Those required to report under Chapter 2M of the Corporations Act 2001 and meet prescribed size thresholds.

- Phasing: Over 3-years commencing 1 July 2024 based on size, subject to submission feedback on a potential 6-month deferral to

1 January 2025.

- Reporting basis: As required by Australian Sustainability Reporting Standards (ASRS). Group 3 entities would only be required to make climate-related financial disclosures if they are subject to material climate-related risks or opportunities for the financial reporting period. Where Group 3 entities assess that they do not have material climate-related risks or opportunities, they would only be required to disclose a statement to that effect.

- Reporting deadlines: A sustainability report forms part of an entities’ annual report and is subject to the same relevant annual financial reporting timetable.

- Assurance requirements: Phased approach commencing with the limited assurance of Scope 1 and 2 emission disclosures from years beginning 1 July 2024 and ending with reasonable assurance of all climate-related financial disclosures from years beginning 1 July 2030.

- Liability framework: 3-year modified liability approach to disclosures of Scope 3 emissions and climate-related forward-looking statements.

Treasury's exposure draft is open for public comment until 9 February 2024.

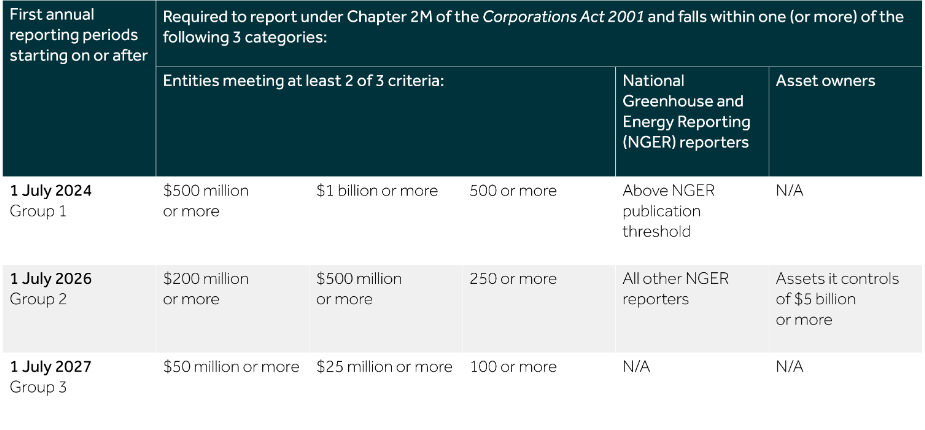

Reporting entities and phasing

3 categories of entities will be subject to mandatory climate-related reporting.

These are entities that are required to prepare an annual report under Chapter 2M of the Corporations Act, and either:

- Meet at least 2 of 3 large criteria. This includes listed and unlisted companies and financial institutions as well as registrable superannuation entities, registered investment schemes, and Corporate Collective Investment Vehicles (CCIV); or

- Are subject to emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007 (NGER Act), regardless

of size; or

- Other entities (such as registrable superannuation entities, registered schemes, and CCIVs) that control assets of more than $5 billion.

Entities below the relevant size thresholds and those that are exempt from preparing financial reports under Chapter 2M of the Corporations Act, including where exemptions have been made through ASIC class orders or where the entity is registered with the Australian Charities and Not-for-profits Commission, will not be required to make climate-related financial disclosures.

A large company limited by guarantee with annual (consolidated) revenue of $1 million or more required to prepare an annual financial report is only required to prepare climate-related information if it also meets any of the other sustainability reporting thresholds.

Reporting of climate-related information will be introduced on the following phased basis:

The proposed commencement date for Group 1 entities is 1 July 2024. Treasury is seeking feedback on whether delaying the commencement date for Group 1 entities until 1 January 2025 would improve the quality of reporting during the transition year.

Consolidated entities

The sustainability reporting requirements apply to each entity that satisfies the above criteria. However, if a parent entity is required by accounting standards to prepare consolidated financial statements, it may choose to prepare its sustainability report also on a consolidated basis. In this case, each other group entity that is otherwise required to prepare a sustainability report would not need to, provided the consolidated sustainability report covers those individual entities.

Reporting requirements

A company’s annual report will now comprise 4 separate reports:

- A Director’s Report;

- The Financial Report, comprising the financial statements, notes to the financial statements, and a directors’ declaration on the statements and notes;

- A Sustainability Report, comprising the climate statements, notes to the climate statements, and a directors’ declaration on the statements and notes; and

- Auditor’s Reports.

Climate statements will be prepared based on sustainability standards issued by the Australian Accounting Standards Board (AASB). The AASB published its draft standard SR1 Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information

in October 2023.

Group 3 materiality exemption

Group 3 entities will be required to make climate-related financial disclosures if they face material climate-related risks or opportunities during the financial reporting period. Materiality will be assessed in accordance with the sustainability standards.

Where Group 3 entities assess that they do not have material climate-related risks or opportunities, they would only be required to disclose a statement to that effect.

Sustainability reporting dates

Because a sustainability report forms part of an entities' annual report, the timing of lodgement of the sustainability report with ASIC and reporting to members will follow the current annual financial reporting timing requirements.

Under section 319 of the Corporations Act disclosing entities and registered managed investment schemes are required to lodge their financial report with ASIC within 3-months after the end of the financial year, and all other companies within 4-months after the end of the

financial year.

The sustainability report must be sent to members and, where relevant, considered at an entity’s Annual General Meeting, in accordance with the relevant timing requirements for the annual financial report.

Assurance requirements

Climate disclosures will be subject to similar assurance requirements to those currently applicable in the Corporations Act for financial reports and will require entities to obtain an assurance report from their financial auditors.

The Australian Auditing and Assurance Board (AUASB) is developing a pathway for phasing in assurance requirements over time, which would commence with limited assurance of Scope 1 and 2 emissions disclosures from years commencing 1 July 2024 and end with reasonable assurance of all climate disclosures from years commencing 1 July 2030.

Auditor independence requirements apply equally to a company’s financial report and sustainability report.

Liability framework

Climate disclosures will be subject to the existing liability framework under the Corporations Act and Australian Securities and Investments Commission Act 2001 including: director’s duties, misleading and deceptive conduct provisions, and general disclosure obligations. This is designed to ensure directors engage fully with their climate disclosure obligations.

Entities will be provided relief for a 3-year period for disclosures relating to Scope 3 emissions and certain forward-looking climate-related statements. For reports issued between 1 July 2025 and 30 June 2028, only the regulator will have the authority to bring action relating to breaches of relevant provisions relating to disclosures of Scope 3 emissions and climate-related forward-looking statements. The remedies accessible to the regulator during this period will be restricted to injunctions and declarations.

Beyond this period, the existing liability framework under the Corporations Act and the Australian Securities and Investments Commission Act

will apply.

Next steps

Talk to your trusted Nexia Edwards Marshall Advisor if you have any questions about the matters discussed in this article.