We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Apr 10, 2024 / News

New tax disclosures in financial reports

The Treasury Laws Amendment (Making Multinationals Pay Their Fair Share – Integrity and Transparency) Act 2024 amends the Corporations Act 2001 to enhance transparency around tax residency of entities within a consolidated group.

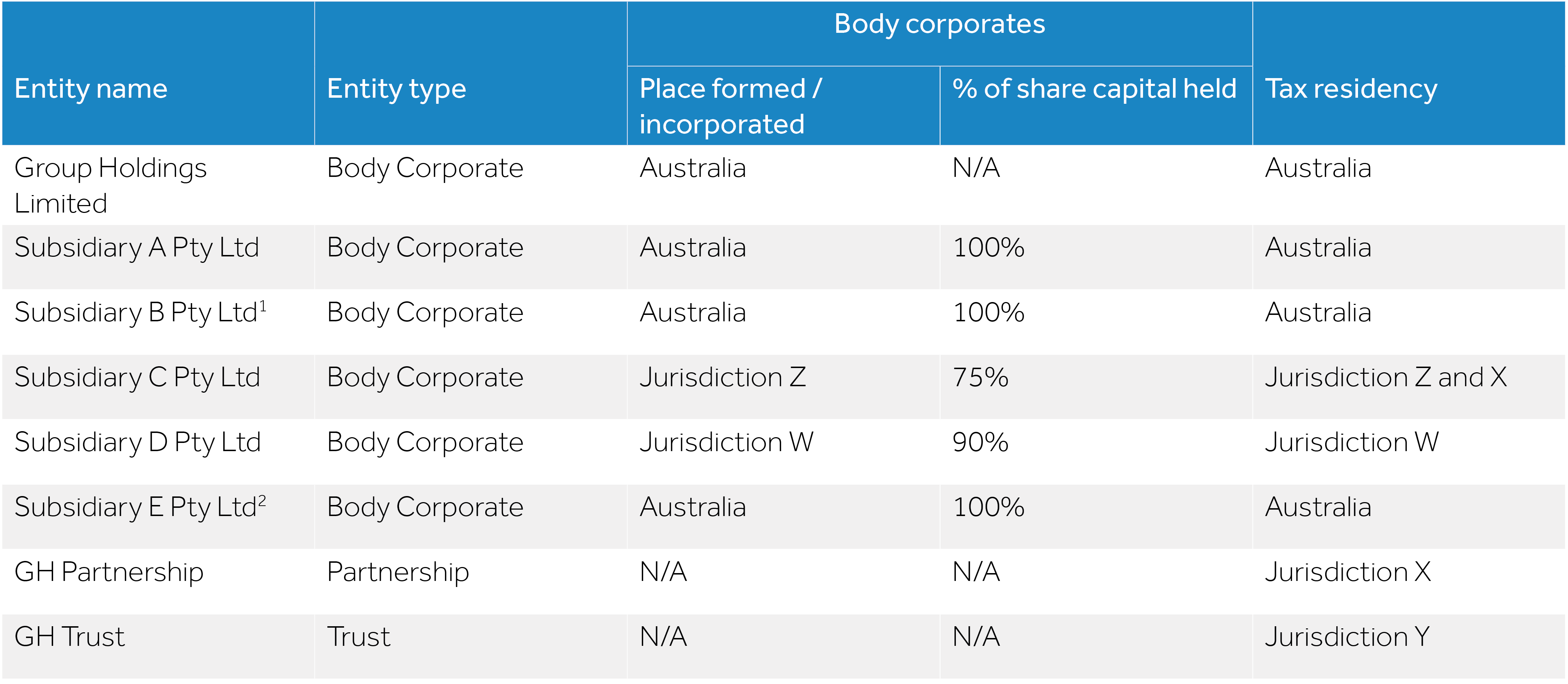

It requires Australian public companies, as part of their annual financial reporting obligations under Chapter 2M of the Corporations Act, to include a ‘Consolidated Entity Disclosure Statement’ describing for each entity that was, at the end of the financial year, part of the consolidated group:

- The entity’s name;

- Whether the entity is a body corporate, partnership or trust;

- Whether the entity was a trustee of a trust within the consolidated entity, a partner in a partnership within the consolidated entity, or a participant in a joint venture within the consolidated entity;

- Where the entity was incorporated or formed (if the entity is a body corporate);

- Where the entity is a body corporate with share capital, the percentage of the entity’s issued share capital held directly or indirectly by the public company;

- Whether the entity was an Australian resident or a foreign resident within the meaning of the Income Tax Assessment Act 1997; and

- If the entity was a foreign resident, a list of each foreign jurisdictions in which the entity was a resident for the purposes of the law of the foreign jurisdiction.

Example disclosure

Group Holdings Limited

Consolidated entity disclosure statement as at 30 June 2024

1Subsidiary B Pty Ltd is a partner in the GH Partnership, which is consolidated within the consolidated financial statements.

2Subsidiary E Pty Ltd is the trustee of the GH Trust.

Large proprietary companies, registered schemes, and other entities that are not public companies are outside of the scope of this requirement. Public companies that do not report under Chapter 2M are also outside the scope of these amendments (for example, charities that report annually to the Australian Charities and Not-for-profits Commission rather than under Chapter 2M).

Where a public company is not required to prepare consolidated financial statements - for example, because it is exempted by AASB 10 Consolidated Financial Statements or because it has no subsidiaries - a Consolidated Entity Disclosure Statement is still required. However, that statement would only note that fact.

The Consolidated Entity Disclosure Statement is a separate statement that forms part of the company’s financial report and is separate from the financial statements. Consequently, it is not made as a note to the financial statements.

The existing directors’ declaration will include a statement about whether, in the directors’ opinion, the Consolidated Entity Disclosure Statement is true and correct.

In addition, for listed public companies, the chief executive officer and chief financial officer will include a statement in their declaration to the directors that the Consolidated Entity Disclosure Statement is true and correct.

The Consolidated Entity Disclosure Statement will be subject to audit.

The inclusion of a Consolidated Entity Disclosure Statement applies to those public companies for financial years commencing on or after 1 July 2023.

Next steps

For further information, talk to your trusted Nexia Edwards Marshall Advisor about how we can help you navigate the often complex relevant accounting and financial reporting standard changes or if you have any questions about the matters discussed in this article.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.