We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Aug 09, 2022 / News

Not For Profit Newsletter

Welcome to the newest edition of our Not-for-Profit Newsletter. Please feel free to contact us if you have any questions about the content of this Newsletter.

In this edition

This edition covers important changes to financial reporting requirements for charities around financial statement disclosures, reporting thresholds, key focus areas and lodgement extensions. We have also included a reminder of the Director Identification Number requirements. There are also a number of items relating to various governance and compliance matters, and ACNC publications and activities.

Click on one of the Newsletter sections below to Scroll to the Section:

Guidance on risk released

A new guide has been released by the Governance Institute of Australia outlining the importance of an integrated approach to risk management. It is designed to be a practical resource to assist Australian directors in any sector.

Risk management for directors: A guide revises its 2016 risk publication, addressing the challenges boards and directors can expect in coming years and how to address best some of the current ones.

It examines risks associated with digital technology, environmental, social and governance considerations, issues uncovered by the aged-care royal commission, and recovery from the pandemic.

It is intended to help boards to integrate their surveillance of governance and risk-management. This should assist organisations to achieve strategic focus by providing boards with the information they need and ensuring risk ownership by employees.

The guide covers:

- An integrated approach to risk management

- The regulatory environment

- Shareholder and member interest in board overseeing of risk management

- Distribution of responsibility

- Board committees — audits and risks

- Culture

- Tools, processes, and improvements

- Non-financial and emerging risks, and

- When risk management fails.

The guide may be accessed at the institute’s website.

Minimum wage increases announced

The Fair Work Commission has reminded employers that new national minimum-wage increases announced on 15 June have come into effect.

From 1 July, wages will increase as follows:

- The minimum wage for award-free employees will be $21.38 an hour or $812.60 a week (an increase of 5.2 per cent), and

- Minimum award rates for award-covered employees will increase by 4.6 per cent for individuals who earn at least $869.60 a week. Those who earn below this will increase their wage by $40 a week.

The commission reminds employers to update their pay practices, including those affecting employees on annualised salaries. With such a significant award increase, annualised salaries might no longer cover award entitlements.

Super guarantee changes

From 1 July, employees have been eligible for super guarantee regardless of how much they earn. The $450 a month eligibility threshold for super-guarantee payments has been removed.

Workers under 18 who do more than 30 hours a week need to be paid super.

The super-guarantee rate increased from 10 per cent to 10.5 per cent on 1 July. You’ll need to use the new rate even if some or all of the pay period is for work done before 1 July.

The super-guarantee rate is legislated to increase to 12 per cent by 2025.

Payroll and accounting systems must be updated to pay correct super amounts.

Director ID deadlines loom

Directors of charities that are companies or Aboriginal and Torres Strait Islander corporations must apply for director identification numbers.

A director ID is a unique 15-digit identifier that is acquired once and kept forever.

Deadlines are:

- Intending new directors under the Corporations Act must apply before appointment

- New directors appointed for the first time between 1 November last year and 4 April should have applied already – they had 28 days from their appointment to apply, and

- While those appointed on or before 31 October last year have until 30 November this year to apply, they are strongly encouraged to do it now.

Directors of an Aboriginal or Torres Strait Islander corporation registered under the Corporations (Aboriginal and Torres Strait Islander) Act 2006 have longer to apply.

Application involves several steps, including verifying your identity, which requires a myGovID.

For more information about who needs to apply and when, including a list of key dates, visit the Australian Business Registry Services website.

Audit committees need plans

The Institute of Internal Auditors in Australia has issued a timely Factsheet: Audit Committee Work Plan.

Work plans amount to what audit committees do over a period – usually a year.

Without one, an audit committee:

- Is operating in an ad hoc way and does not have a structured approach to its work

- Will not know if it has covered the range of governance and assurance activities required to do its job properly, and

- Will generally have its agenda determined by management – an audit committee should be setting its own agenda.

The guide can be accessed at the institute’s web site.

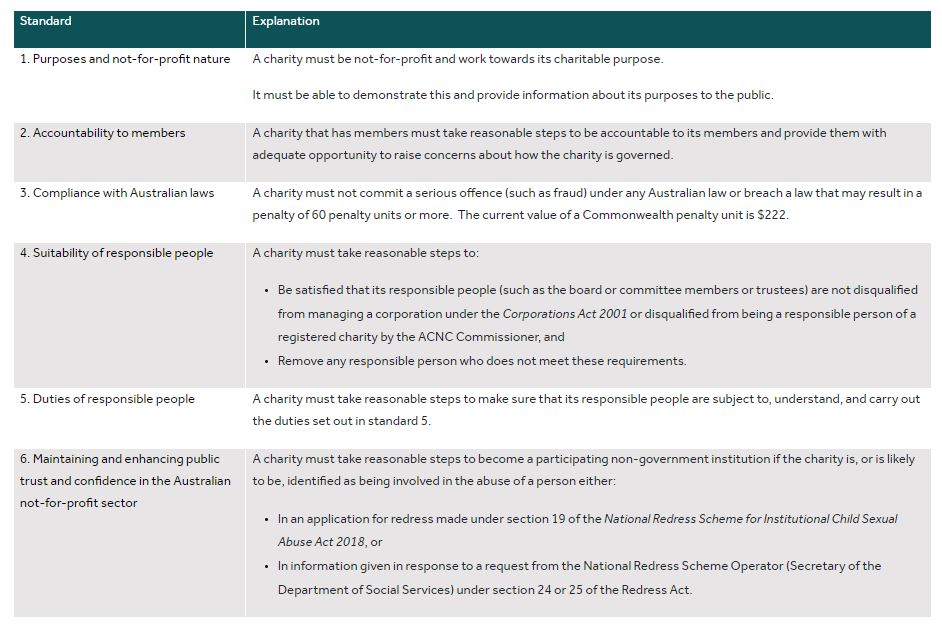

Adhering to governance standards

The Australian Charities and Not-for-profits Commission governance standards is a set of core principles dealing with how a charity should be run.

Charities must meet the standards to be registered and remain registered with the ACNC. The principles do not apply to basic religious charities.

They require charities to remain charitable, operate lawfully, and be run in an accountable and responsible way. They help to maintain public trust in charities.

The principles are high-level, not precise rules, and charities must determine what they need to do to comply with them.

The ACNC’s self-evaluation tool aims to help charities assess if they are meeting their obligations. It also helps to identify issues that might prevent them from doing so.

It poses questions and prompts charities to describe both the practical steps they are taking to meet their obligations, and to list the relevant policies or procedures.

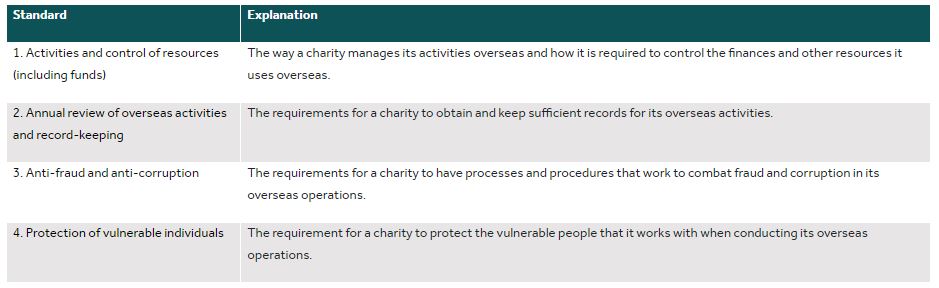

A charity that conducts activities overseas – including sending funds overseas from Australia – must also comply with external-conduct and governance standards.

Four external-conduct standards cover certain aspects of a charity’s overseas operations.

An ACNC self-evaluation tool for charities operating overseas aims to help charities assess if they are meeting their obligations and identify issues that might prevent them from doing so.

The tool poses questions and prompts charities to describe both the practical steps they are taking to meet their obligations.

Charity-sector insights

The latest Australian Charities Report details Australian charities’ contribution to the economy and communities.

In the 2020 reporting period:

Employment

- Charities employed 10.5 per cent of Australian employees – 1.38 million people

- There was a rise in the proportion of full-time and part-time staff

- Education charities employed the most staff – more than 330,000

- Volunteer contribution was high at 3.4 million, but decreased by 220,000 on the previous period

- 51 per cent of charities reported no paid staff

- Environment charities reported the most volunteers – 810,000, and

- About half of the sector’s expenses were employee expenses

Revenue

- Charities’ revenue rose to $176 billion – up by more than $10 billion on the previous period

- Donations rose by 8 per cent to $12.7 billion

- Revenue from government rose to $88.8 billion – up $10.7 billion on the previous period, accounting for 50.4 per cent of total revenue

- Other major revenue sources were goods and services (32.5 per cent) and donations or bequests (7.2 per cent), and

- The 50 largest charities by revenue accounted for 33 per cent of total sector revenue

Expenses

- Expenses increased by $10.2 billion.

The report is based on data that 49,000 charities submitted in their 2020 annual information statements – most reporting on the 2020 calendar year or the 2019 –20 financial year.

JobKeeper payments to ACNC-registered charities supported an estimated 331,000 individuals between April and September 2020. This reduced to about 128,000 individuals between October and December 2020, and 86,000 between January and March 2021.

For the first time, the report has collected ‘program’ data, giving an insight into the work of the sector across 75,000 programs. About 7 per cent of charities reported that they operated overseas. Some 217 countries or regions were named. The five most common were Cambodia, the Philippines, Indonesia, Kenya, and Papua New Guinea.

Charities under the microscope

The ACNC has reviewed registered charities to ensure that their records are accurate and only eligible charities are listed.

The initiative began in 2020-21 by examining 303 charities that were also public benevolent institutions and were missing information on their charity-register record – such as governing documents and responsible people.

The commission examined these charities to assess their eligibility to remain registered as PBIs and, where necessary, provided guidance to assist them to meet their obligations.

Where this was not possible, the ACNC revoked registration or access to specific charity subtypes. Most of the charities whose registrations were revoked (52 per cent did so voluntarily) were found to be no longer operating or government entities.

Sometimes new case law might have affected registration. Sometimes a charity’s purpose was not charitable.

Of the initial 577 higher-risk charities reviewed the commission found that:

- 13 per cent required no follow up

- 15 per cent had administrative concerns about registration obligations, the ACNC following up by sending them guidance, and

- 72 per cent had potential entitlement concerns and either had been or would be subject to a more detailed review.

Other administrative reviews, which covered all registered charities, identified:

- 248 charities with cancelled Australian business numbers

- 125 incorrectly reporting as basic religious charities

- 2470 without an appropriate governing document, and

- 2513 with information withheld from the charity register.

The commission also identified charities that did not have any responsible people listed on the register or did not appear to have an appropriate number listed.

Seeking comment on PBI and HPC

The ACNC is seeking public comment on two updated commissioner’s interpretation statements, aiming to ensure that they are clear and accurately reflect the law.

They are:

- Commissioner’s statement on public benevolent institutions, and

- Commissioner’s statement on health-promotion charities.

Public comment is allowed until 30 August.

Hundreds of charities lose registration

Almost 400 charities that have failed to submit two or more annual information statements have lost registration.

ACNC assistant commissioner general counsel Anna Longley said many of the 396 organisations that have had registrations revoked were likely to have stopped operating.

‘Information that we publish on the register is largely provided by charities in their [statements], so timely AIS submission is very important. If a charity has ceased operating or is not meeting its reporting obligations, it loses ACNC registration and eligibility for certain Commonwealth tax concessions that are available only to registered charities,’ said Ms Longley.

‘In April, the ACNC notified almost 750 organisations that they risked revocation. ‘Those organisations that are still operating have been provided every opportunity to retain registration. Over the past few weeks, many have submitted their overdue statements and continue to be registered.’

ACNC extends AIS deadline for flood-affected charities

Following recent floods in parts of the New South Wales disaster zone, the ACNC is granting affected charities an automatic extension on their annual reporting deadlines.

Twenty-three local government areas have been affected by severe floods.

Charities in affected postcodes with a reporting period that ends between January and April will automatically be granted an extension to 31 October to submit their 2021 information statement.

Remake of ACNC regulations

The existing Australian Charities and Not for profits Commission Regulations 2013 is set to end on 1 April next year.

A draft Australian Charities and Not for profits Commission Regulations 2022 proposes minimal changes.

Minor amendments reflect current drafting practices, improve clarity, and remove provisions such as transitional reporting arrangements that are no longer required.

Views are sought on the draft regulations and an explanatory statement.

SD replaces RDR

The Australian Accounting Standards Board has developed a new simplified-disclosure standard to replace reduced-disclosure requirements.

AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities, a new simplified disclosure standard based on IFRS for Small and Medium-sized Entities, to replace the RDR. These simplified disclosure requirements are now collated in a single disclosure standard.

The 98-page AASB 1060 applies to reporting periods ending 30 June for the first time.

The standard sets out a separate disclosure standard to be applied by entities reporting under Tier 2 of the differential reporting framework in AASB 1053 Application of Tiers of Australian Accounting Standards.

Importantly, AASB 1060 does not change which entities are permitted to apply Tier 2 reporting requirements. Recognition and measurement requirements for Tier 2 are the same as for Tier 1.

Disclosures relevant to Tier 2 entities are set out in AASB 1060. Disclosure requirements in the body or appendix of other standards will no longer be shaded or unshaded in relation to Tier 2 requirements.

While entities that comply with this standard need to apply recognition and measurement requirements of other standards, they are exempt from disclosure requirements in specified paragraphs of other standards.

Tier 2 entities are also not required to comply with other standards that deal only with presentation and disclosure.

Charity thresholds change

Reporting and assurance thresholds will change in 2022 annual charity statements. For many charities, this will apply to the reporting period between 1 July last year and 30 June.

The table below compares old and new revenue thresholds for small, medium, and large charities.

While thresholds have changed, the following should also be considered:

- Check governing documents to see if an audit is required. If an audit is required, then the changes to thresholds have no effect unless governance documents are amended

- If a review has become an option, consider whether this lower level of assurance provided by your auditor meets your needs and those of report users, and

- If a review is no longer required, consider how the lack of any firm assurance will affect your compliance obligations with governance standards and relationships with external stakeholders.

What is revenue?

Revenue determines reporting thresholds, and the ACNC has provided the following definition.

‘Revenue is a component of total income. A simple formula to help charities understand this is: Revenue + Other Income = Total Income.’

Revenue is realised from the sale of goods and services or through the use of capital and assets. Revenue can also arise from the contribution of an asset to a charity when certain conditions have been met during the charity’s ordinary activities.

Revenue is usually shown as the top line item in an income (profit and loss) statement.

Common examples for charities include:

- Grants from government, foundations, private and any other sources

- Donations, tithes, bequests, and legacies

- Fees for provision of services

- Sale of goods

- Inflows from fundraising activities and sponsorship

- Interest earned on investments and dividends

- Royalties and licence fees, and

- In-kind donations (for example, volunteer time and goods).

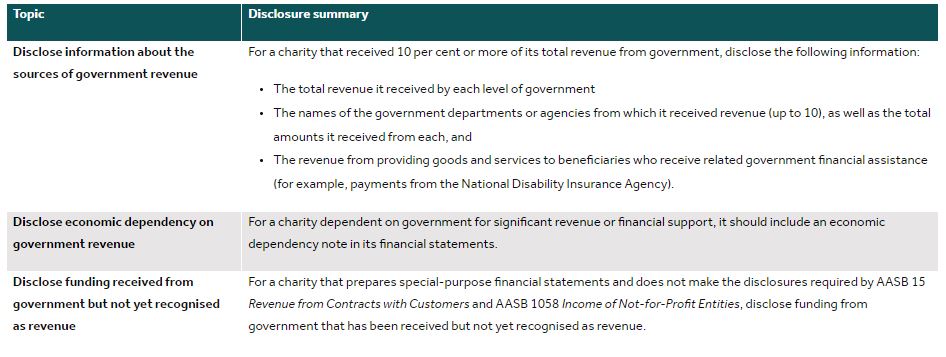

Best practice disclosure for government funding

Government funds are a significant source of revenue for many charities. Reports have repeatedly shown that nearly half of the charity sector’s revenue comes from government.

Whether a charity has received funds from governments and others, the amounts and sources interest donors, funders, supporters, and the public.

The ACNC has recommended three best-practice disclosures of government funding in a charity’s annual financial report.

Examples illustrate NFP amendments

AASB 2022-3 amends Australian illustrative examples for NFPs accompanying AASB 15 Revenue from Contracts with Customers. The amendments do not change AASB’s requirements.

Example 7A illustrates how AASB 15 applies to the recognition and measurement of upfront fees charged to customers and members.

The guidance explains that where the goods or services to which the upfront fee relates are in the scope of AASB 15, the recognition of the upfront fee as revenue depends on whether the payment of the fee relates to a transfer of distinct goods or services to the customer that meets the definition of a performance obligation.

In many cases, even though a non-refundable upfront fee relates to an activity that an entity is required to undertake to fulfil a contract, the action may be an administrative task that does not necessarily result in the transfer of a promised good or service to the customer.

The basis for conclusions accompanying AASB 2022-3 documents the AASB’s decision to retain the accounting-policy choice for NFP private-sector lessees who might elect to measure initially a class of right-of-use assets arising under concessionary leases at cost or at fair value.

The board has deferred consideration of accounting-policy choice for NFP public-sector lessees until it decides on any additional guidance for measuring the fair value of right-of-use assets under concessionary leases.

AASB 2022-3 applies to annual reporting periods beginning on or after 1 July.

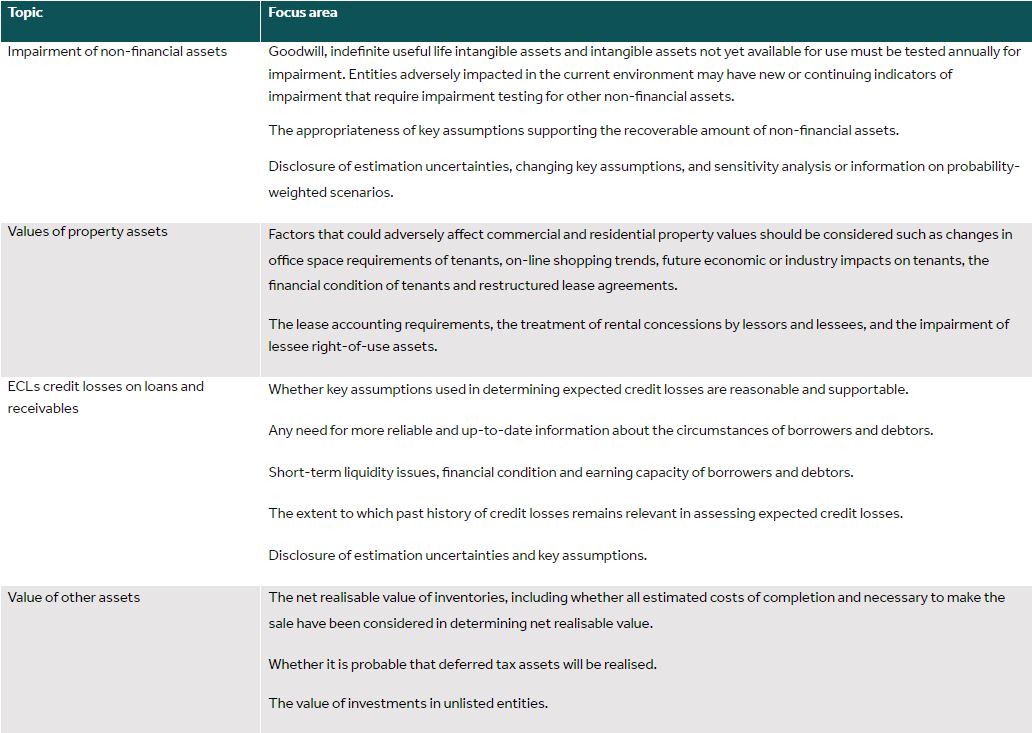

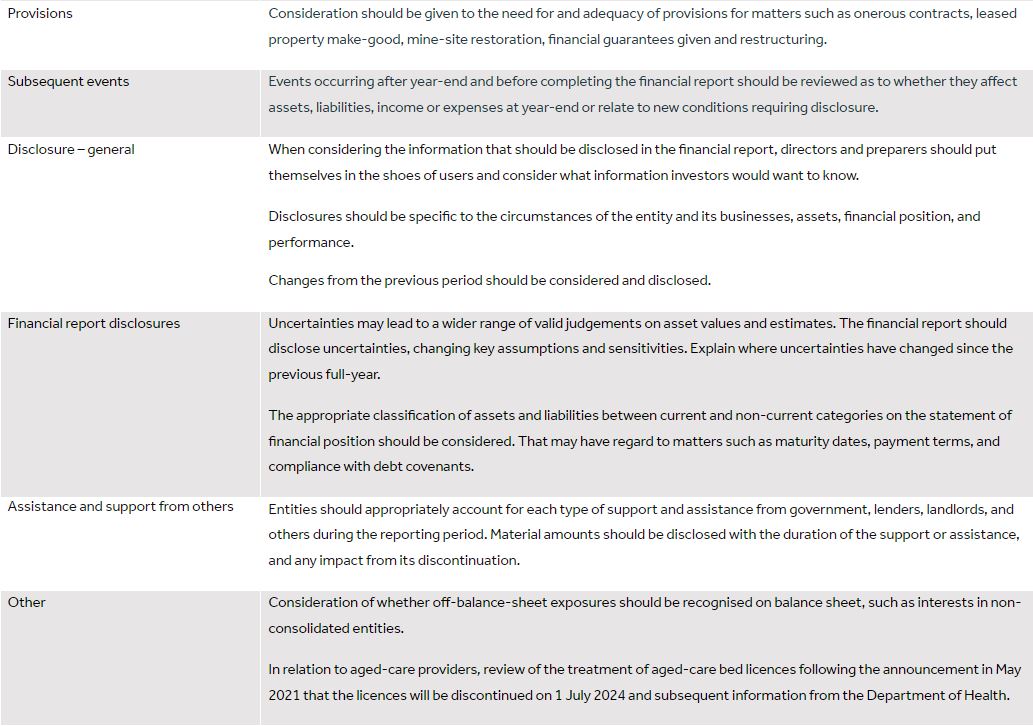

ASIC highlights key reporting areas

The Australian Securities & Investments Commission is urging directors, report preparers, and auditors to assess whether financial reports provide useful and meaningful information.

The commission has highlighted key areas for companies to get right for the 30 June year-end. While NFPs have not been specifically mentioned, many of the focus areas are relevant to them.

Among them are asset values, provisions, solvency, and going-concern assessments. Events occurring after year-end and before completing reports will also be examined.

Companies may continue to face uncertainties about future economic and market conditions – assumptions underlying estimates and assessments for reporting purposes should be reasonable and supportable.

Directors and management should assess how current and future company performances, the value of assets, provisions, and business strategies might be affected by changing circumstances, uncertainties, and risks such as:

- COVID-19 conditions and restrictions

- Use of virtual meetings and more flexible working arrangements

- The discontinuation of financial and other support from governments, lenders, and lessors, including possible increases in insolvency levels

- The availability of skilled staff and expertise

- Restrictions to deal with COVID-19 in different jurisdictions, and

- The impact of rising interest rates on future cash-flows and on discount rates used in valuing assets and liabilities.

Uncertainties might lead to a wider range of valid judgements on asset values and other estimates. Uncertainties might also change. Disclosures in financial reports about uncertainties, key assumptions, and sensitivity analysis will be important.

Appropriate experience and expertise should be applied in reporting and auditing, particularly in more difficult and complex areas such as asset values and other estimates, ASIC says.

Directors and auditors should be given sufficient time to consider reporting issues and to challenge assumptions, estimates, and assessments.

They should make appropriate enquiries of management to ensure that key processes and internal controls have operated effectively during periods of remote work.

The circumstances in which judgements on accounting estimates and forward-looking information have been made and the basis for those judgements should be properly documented and disclosed as appropriate, the commission says.

For details below:

ASIC extends deadlines for some 30 June financial reports

ASIC extended the deadline for unlisted entities to lodge financial reports by a month for balance dates from 24 June to 7 July.

The extended deadlines are intended to help relieve pressure on resources for reporting and audits by smaller entities, considering challenges presented by COVID-19.

ASIC said it recognised that companies and audit firms might have reduced staff numbers due to varying travel restrictions and increased resignations in the past two years. Higher staff absences were also expected.

Some companies were also required to prepare consolidated financial statements for the first time, and judgements on asset values, provisions and disclosures might be more difficult given changed economic conditions.

Directors of some unlisted companies may be asked by their auditors to facilitate the spreading of deadlines for lodging audited financial reports. Directors should consider the information needs of shareholders and other users of their financial reports, as well as meeting borrowing covenants or other obligations, when deciding whether to depart from the normal statutory deadlines.

ASIC will consider relief for other entities and balance dates on a case-by-case basis.

An instrument that amends ASIC Corporations (Extended Reporting and Lodgement Deadlines—Unlisted Entities) Instrument 2020/395 to extend the deadlines is expected to be registered on the Federal Register of Legislation by the end of July.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.